The Map to Asset-Grade

Prediction markets are scaling faster than their market structure. That gap is where every failure in this category is coming from, and unless it closes, institutional adoption will stall exactly when the capital is accelerating.

Three months ago, a short piece ran on this desk arguing that prediction markets going mainstream without market-grade integrity controls was gambling wearing an investment-grade wrapper. Joseph Saluzzi extended the argument with a sharper version focused on what happens when these instruments get packaged into ETF wrappers and pulled into the broader brokerage ecosystem. The exchange surfaced the question this piece sets out to answer.

Since then, the category has not slowed down for the debate. Polymarket cleared another five billion in volume. ICE committed two billion dollars to the platform. Kalshi crossed an eleven-billion-dollar valuation. The Department of Justice dropped its investigation into Polymarket in July. In October, Polymarket's acquisition of QCX secured its CFTC-registered path back into the United States.

The moment institutional capital shows up is the moment market structure becomes non-optional. That moment is now.

So the question posed in December has a different shape. It is no longer whether prediction markets should exist at institutional scale. That question has been answered by capital. The question is whether the venues operating them will build the microstructure the category needs to become actual financial infrastructure, or whether they will be forced into it retroactively by regulators and the cost of their own integrity incidents.

This piece is the map.

One thing first, directly: most prediction markets today are not markets. They are thinly structured order books pricing binary risk without the controls required to survive informed flow. That is a serviceable description of a sports betting site. It is not a description of financial infrastructure. The distinction matters because the category is claiming the latter while operating as the former, and the next eighteen months will decide which one it actually becomes.

At Sapinover, we study prediction markets as global risk signals. How overnight price formation on binary event contracts interacts with the rest of the system. Whether a platform that prices the probability of a ceasefire in real time is giving institutional risk managers information they cannot get anywhere else. The answer is yes, but only when the plumbing works.

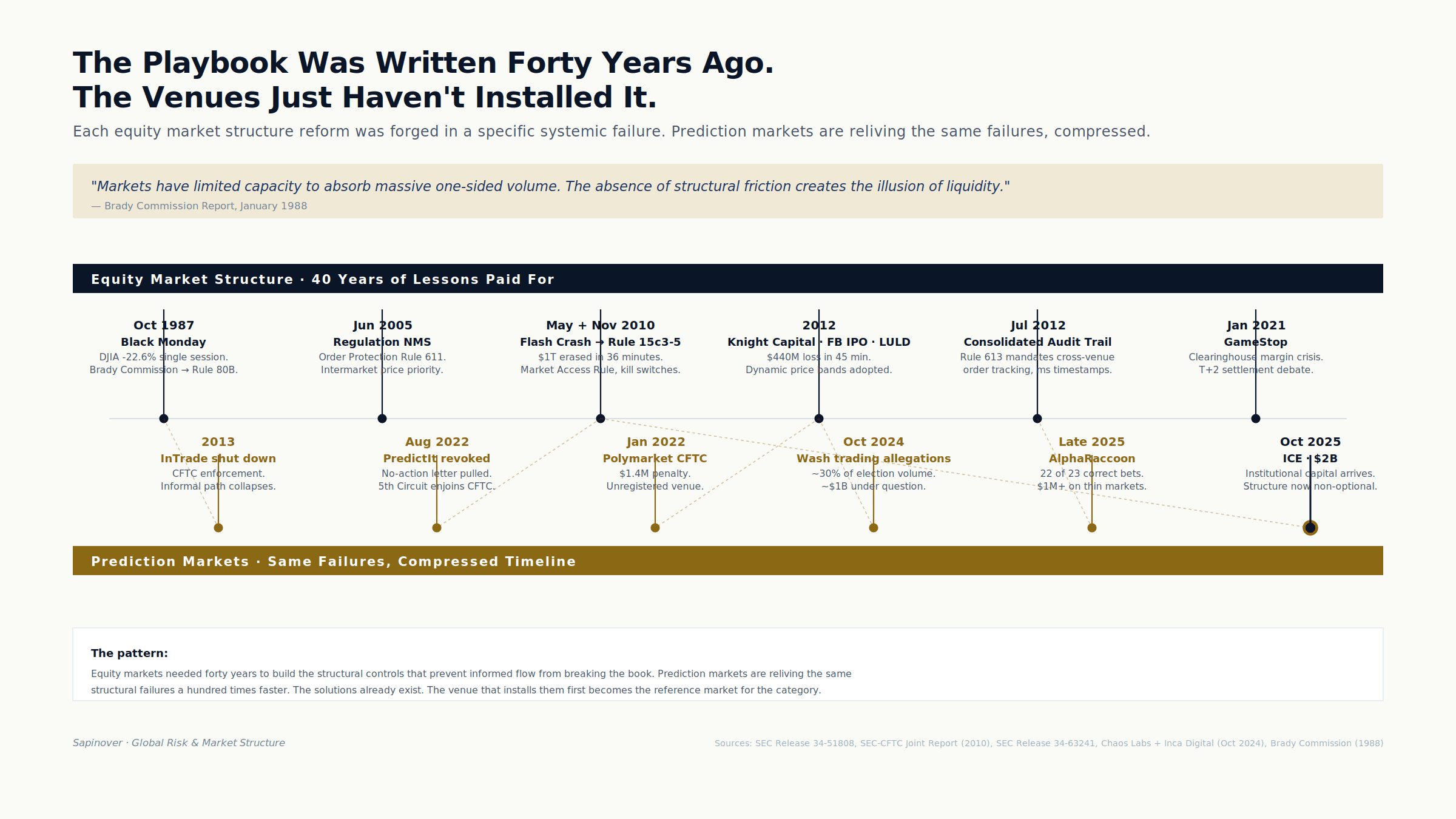

Every major incident prediction markets have faced in the last eighteen months has been a market structure problem mislabeled as something else. The AlphaRaccoon run on Google's Year in Search. The one billion dollars in wash trading allegations around the 2024 U.S. presidential election. The contested resolutions on edge-case events. These are not the pathologies of an emerging asset class. They are the predictable structural failures of venues that scaled their market count a hundredfold without upgrading the infrastructure underneath.

Equity markets faced every one of these problems. They spent forty years solving them. Prediction markets do not have forty years. The regulators are already writing the next rules. ICE's operational team is already reading for them. The venue that builds the playbook first will define the terms the rest of the category gets measured against.

Here is what the playbook looks like.

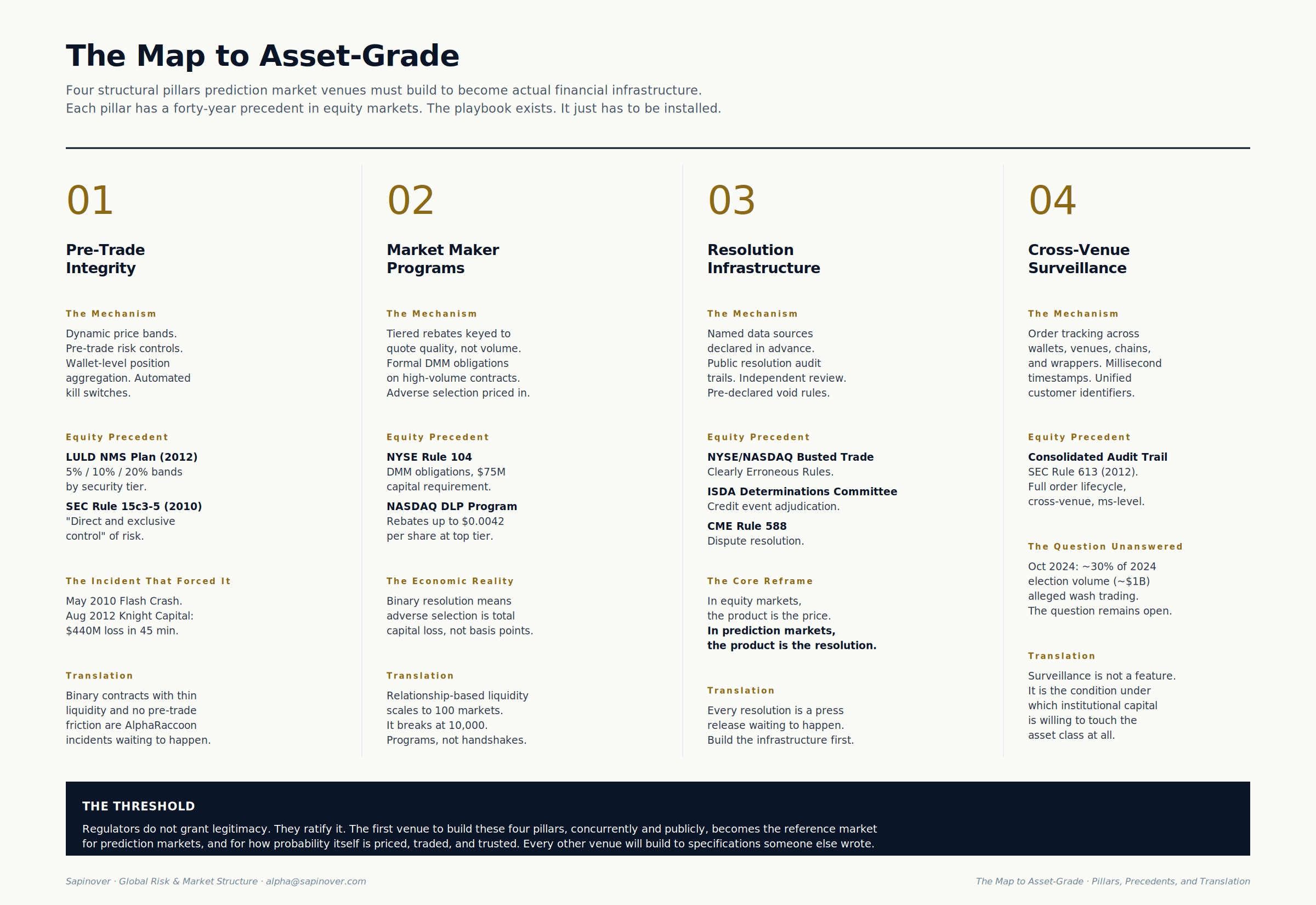

01Pre-Trade Integrity: The Brady Report Was Always About This

In January 1988, the Brady Commission published its postmortem on the October 1987 crash. Twenty-two percent of the Dow erased in a single session. The commission's conclusion was blunt: markets have “limited capacity to absorb massive one-sided volume,” and the absence of structural friction created the “illusion of liquidity” that collapsed the moment informed flow arrived at scale.

That 1988 paragraph describes the AlphaRaccoon incident perfectly.

A single trader, armed with apparent non-public information about Google's Year in Search rankings, placed twenty-two correct bets out of twenty-three. The market absorbed over a million dollars in one-sided informed volume across thin binary contracts with no pre-trade friction. The Brady Commission wrote the playbook for this in 1988. They were talking about portfolio insurance and they were also talking about this. The solution is thirty-seven years old. The venues just have not installed it yet.

It is worth engaging directly with the counterargument. A robust academic literature, led by Hanson, Oprea, and Porter, demonstrates that in controlled settings, manipulation attempts in prediction markets fail. Informed arbitrageurs trade against the artificial pressure and rapidly return prices to equilibrium, extracting the manipulator's capital in the process. The finding is real and worth preserving. It also describes a market structure that prediction markets often do not have on the long tail of thin, esoteric contracts. The arbitrage-punishes-manipulation equilibrium requires thick markets, sophisticated counter-trading capital, and speed. Structural friction is not an alternative to arbitrage. It is what keeps the arbitrage window open long enough for arbitrageurs to arrive at size. Frictionless thin markets are not self-correcting. They are AlphaRaccoon waiting to happen.

Equity markets learned this the hard way, twice. The first time produced NYSE Rule 80B in 1988, imposing market-wide trading halts. The second time, after the May 2010 Flash Crash erased a trillion dollars in thirty-six minutes, produced the Limit Up/Limit Down NMS Plan. LULD replaced single-stock pauses with dynamic price bands, tiered by security classification. Tier 1 securities trade within five-percent bands during regular hours. Tier 2 securities within ten percent. The bands double during the opening fifteen minutes and the closing twenty-five minutes, the periods when informed flow is most likely to hit. LULD does not prevent price discovery. It prevents the seven-seconds-to-zero cascade that makes markets unusable for institutional participants.

Sports betting exchanges solved an adjacent version of this problem with what operators call the VAR rule. On Betfair, when a Video Assistant Referee decision materially alters a match outcome, the matching engine retroactively voids all bets executed during the latency window between the real-world event and the official data feed update. The rule exists because latency-arbitrage snipers could otherwise guarantee risk-free profits by exploiting the temporal gap between physical reality and the venue's knowledge of it. The VAR rule is a working production precedent for time-window protections in event-driven markets. Prediction markets face the same latency problem on every information event. The precedent exists. It operates at scale.

The second pillar of pre-trade integrity is SEC Rule 15c3-5, the Market Access Rule adopted in November 2010. The rule eliminated what the industry called “naked access” to exchanges. It requires broker-dealers to maintain financial and regulatory risk controls under their “direct and exclusive control,” with pre-trade limits on credit exposure, capital consumption, and regulatory compliance. The rule's teeth are in its kill-switch requirement: automated systems that must immediately block order entry for any algorithm exhibiting aberrant behavior.

Knight Capital demonstrated what happens when Rule 15c3-5 controls are insufficient. On August 1, 2012, Knight deployed untested code and an old algorithm triggered an infinite loop that executed four million unintended trades across 154 stocks in forty-five minutes. The firm incurred a $440 million pre-tax loss and the SEC imposed a $12 million penalty for failure to maintain pre-trade safeguards. Knight did not survive the incident as an independent firm.

Prediction markets today operate much closer to Knight's pre-controls environment than to the post-Rule 15c3-5 environment. API-driven trading, wallet-level position aggregation, and automated market making interact without the structural circuit breakers that equity markets took a decade to build. The translation: every participant operating at API speed should be subject to pre-trade notional limits, position aggregation across correlated contracts, automated kill switches that trigger on anomalous wallet-level behavior, and VAR-style voiding protections on latency-window executions. This is not optional if the category is going institutional. ICE will require it. The CFTC will require it. Whoever builds it first builds it once.

02Market Maker Programs: AMMs and DMMs, Together

Prediction markets exist as a financial product at institutional scale because Robin Hanson solved the thin-market problem. Traditional continuous double auctions routinely fail when buyers and sellers cannot organically meet at a mutually agreeable price. Hanson's Logarithmic Market Scoring Rule, published in 2003 and formalized in 2007, acts as a sequential automated market maker that serves as universal counterparty to all trades. The LMSR guarantees baseline liquidity at every price level, mathematically bounds the protocol's maximum loss through a liquidity parameter, and allows informed participants to always register their private information into the price. Without LMSR or its modern variants, the long tail of esoteric event contracts would be uninvestable. AMMs are not a design choice prediction markets can abandon. They are the mathematical foundation that makes ten thousand concurrent markets possible in the first place.

But institutional scale requires more than mathematical baselines. It requires depth.

Relationship-based liquidity scales to a hundred markets. It breaks at ten thousand. More precisely: AMM-provided liquidity scales to the long tail, but institutional block sizes on high-volume contracts need something AMMs cannot efficiently provide. A market maker with committed capital, continuous two-sided quoting obligations, and inventory-management discipline. The category's next step is not replacing AMMs. It is layering formal designated market maker programs on top of AMM infrastructure for the high-volume subset of contracts where institutional capital actually wants to execute.

Equity markets answered this problem with formal DMM programs. NYSE Rule 104 obligates designated market makers to maintain continuous two-sided quotes with reasonable depth at the National Best Bid and Offer for a specified percentage of the trading day. DMMs are required to dynamically supply their own capital to dampen volatility when public liquidity fails. The baseline capital requirement is $75 million. In return, DMMs receive rebate structures and specific systemic privileges, including a role in the opening and closing auctions. NASDAQ's Designated Liquidity Provider program uses aggressively tiered rebates keyed to ADV thresholds, up to $0.0042 per executed share at the top tier. CBOE's Lead Market Maker program pays daily stipends from $10 to $100 per security, with obligations for continuous two-sided quotes at maximum spread widths and minimum depth.

The academic literature on liquidity provision, led by Larry Harris, Maureen O'Hara, and Terrence Hendershott, is unambiguous: liquidity is not a byproduct of relationships. It is an engineered outcome of structural incentives aligned against adverse selection. Bruno Biais and Thierry Foucault extended this work to algorithmic markets, showing that speed reduces inventory risk but increases adverse selection. Market makers get picked off by informed traders with superior information or faster connections. The maker-taker rebate exists to subsidize that adverse selection cost.

Prediction markets face a worse version of this problem than equities. A binary contract resolving to zero or one means that being picked off by an informed trader is not a basis-point event. It is total capital loss on the position. The adverse selection cost is existential, not marginal. AMMs absorb this cost mathematically, with the liquidity parameter defining the maximum subsidy the protocol accepts. Human market makers cannot absorb it at all without explicit compensation. Any DMM program on top of AMM infrastructure must price binary adverse selection into the incentive structure from day one, or no professional capital will participate.

The program design for prediction markets needs four elements. First, tiered rebates keyed to quality, not volume: uptime at the best bid and offer, quoted depth at specified spread widths, spread variance measured across rolling windows. Market makers who meet all three get the top tier. Second, explicit position limits preventing concentration risk across correlated contracts. A market maker quoting thirty sports contracts correlated to a single outcome has a different risk profile than one quoting uncorrelated events. Third, formal DMM obligations on the highest-volume contracts, modeled on NYSE Rule 104, with capital requirements and continuous quoting. Not all ten thousand markets need DMMs. The top five percent by volume do. Fourth, and this is where prediction markets have an advantage equity markets never had: the ability to design against the payment-for-order-flow pathology from day one. The PFOF structure in equities segmented order flow, leaving public limit order books saturated with informed toxic flow while uninformed retail flow was internalized off-exchange. Prediction markets are not trapped in that legacy. They can design routing incentives that keep flow on the central limit order book from the start, and they should.

03Resolution Is the Product

Equity markets and prediction markets are both pricing probability. One just admits it.

In equity markets, the product is the price. The venue's core value proposition is continuous price discovery, and everything in the microstructure stack exists to make that price discovery efficient. Fills, spreads, depth, latency.

In prediction markets, the product is not the price. The product is the resolution.

A prediction market contract trades continuously from inception to event. The price during that window is a probability estimate, and it is valuable. But the thing the customer actually bought, the thing they expect the venue to deliver, is a correct and credible settlement at resolution. If the price discovery along the way was perfect but the resolution is contested, the customer does not care about the price discovery. They care that the venue delivered the outcome they paid for.

Every resolution is a press release waiting to happen. The venues that scale will be the ones that built the infrastructure to handle that reality before they needed it.

Equity and derivatives markets have forty years of infrastructure for this. NYSE and NASDAQ clearly erroneous execution rules. CBOE obvious error adjustment procedures. CME Rule 588 dispute resolution for futures. ICE's own dispute mechanisms. The ISDA Credit Derivatives Determinations Committees adjudicate whether a credit event has occurred under a credit default swap. The Greek debt restructuring in 2012 and Argentina's default were live adjudications where billions of dollars of contracts settled on committee decisions. The market did not collapse. The process worked.

It is worth saying what “the process worked” means, because it does not mean the committees were always right. They were not. The ISDA DC structure has been exploited, most notably in the 2017 Hovnanian situation where a manufactured default engineered by creditors forced the committee to rule on a technicality because it had no jurisdiction over intent or good faith. That incident is a cautionary tale about centralized committee design, not an advertisement for it. The lesson is that resolution frameworks need to anticipate bad-faith engineering and build in good-faith provisions, or they become tools for sophisticated counterparties to game. Prediction markets have the advantage of learning this lesson before building their own adjudication structure.

The reason the underlying model still works, despite its flaws, is that the process is transparent, the criteria are published, the decision is defensible, and the venue has pre-committed to a mechanism for handling disputes before the disputes arose. That combination matters more than committee infallibility.

Prediction markets need a resolution framework with four components. Named data sources declared in advance. Polymarket does this well. Every market names its resolution source before the contract is listed. This should be industry-standard, not a Polymarket differentiator. Public resolution audit trails. Every resolution decision should produce a public record documenting the data source, the observed outcome, the timestamp, and the adjudication pathway if the outcome was contested. This is not expensive to build. It is expensive to retrofit. Independent integrity review for contested resolutions, with good-faith and intent provisions baked in to prevent Hovnanian-style manufactured exploits. An independent body with market structure professionals, academic researchers, and regulatory veterans, with explicit authority to examine counterparty intent on contested resolutions. The venues will resist this because it feels like ceding control. They should do it anyway. Predeclared voiding conditions, including latency-window protections modeled on the Betfair VAR rule. Sports betting exchanges have spent twenty years developing this infrastructure. Prediction markets can adopt it directly.

The person running markets at a prediction market venue at scale will spend more time on resolution than on any other single function. That person will be across the table from regulators, journalists, and aggrieved counterparties regularly. The venue that survives will be the one where the answer to every question begins with “here is the pre-committed framework and here is the published decision.”

04Surveillance Is Not a Feature. It Is the Condition.

In October 2024, independent analyses from Chaos Labs and Inca Digital estimated that roughly thirty percent of Polymarket's U.S. presidential election volume, over one billion dollars, was artificial wash trading. Polymarket disputed the methodology. The question of what the number actually was matters less than the fact that the question could be asked and not answered.

Equity markets developed the Consolidated Audit Trail under SEC Rule 613 to answer exactly this kind of question. Every order, modification, cancellation, and execution across all U.S. equities and options, timestamped to the millisecond, tied to a unified customer identifier. The CAT exists because fragmentation made cross-venue manipulation undetectable with siloed data. Spoofing, layering, and wash trading became visible only when regulators could reconstruct the full order lifecycle across every venue simultaneously.

Prediction markets are more fragmented than equity markets ever were. Multiple venues. Multiple chains. Multiple settlement layers. Multiple wrappers, including the ETF structures that are coming whether the plumbing is ready or not. Without cross-venue surveillance, the wash trading question will never be answerable. The insider trading question will never be answerable. The market manipulation question will never be answerable. And the category will remain an asterisk asset class.

The honest realism here is that a globally unified surveillance framework is not achievable in the near term, and anyone claiming it is does not understand the jurisdictional landscape. European jurisdictions prohibit these instruments outright. The UK Gambling Commission classifies them as betting intermediaries rather than derivatives, with a completely separate supervisory regime. Australia bans most consumer access. State-level U.S. gaming regulators are already in tension with federal CFTC authority, and the tension will grow as the category scales. A single unified tape is legally untenable today, and probably this decade.

The achievable goal is different and still transformational. CFTC-regulated jurisdictions build the surveillance standard first, with rigorous documentation, published methodologies, and cooperative bilateral data-sharing arrangements with regulators in aligned jurisdictions. The UK FCA, Singapore MAS, and Canadian provincial regulators have precedent for this kind of bilateral coordination in adjacent asset classes. The venues that lead on the work, even imperfectly and within fragmented jurisdictional reality, shape the eventual international framework.

Surveillance is not a feature venues add to make regulators happy. It is the condition under which institutional capital is willing to touch an asset class at scale.

The firms ICE brings to the table will ask about surveillance in the first meeting. The answer “we self-monitor internally” ends the meeting. The venue that builds a CAT-equivalent surveillance framework first, starting with U.S. jurisdiction and extending through bilateral arrangements, owns the regulatory moat for a decade. This is not a cost center. It is the most valuable piece of infrastructure the category can build.

05The Asset-Grade Threshold

InTrade is the cautionary tale. Launched in 2001, forecasting U.S. elections with remarkable accuracy, shut down by the CFTC in 2013 for offering unregistered off-exchange options. PredictIt is the second cautionary tale. Operated under an informal CFTC no-action letter from 2014, the letter was abruptly revoked in 2022. A federal appeals court eventually enjoined the revocation as likely arbitrary and capricious, but the lesson was delivered: informal regulatory paths collapse at scale.

The third path is the one Polymarket is now on. Formal CFTC registration through the QCX acquisition. ICE as a strategic investor. U.S. institutional data distribution. This is the asset-grade path for U.S. jurisdiction, and it is the only one that works over a ten-year horizon. It does not solve the international fragmentation problem. It does solve the most important piece, which is regulatory standing in the market where institutional capital lives. Registration is a floor, not a ceiling. The venues that achieve registration and stop building are the ones that become regulatory case studies when the next AlphaRaccoon incident hits.

The map to asset-grade is four structural pillars, built concurrently, published publicly, and maintained under the kind of scrutiny equity markets accept as the cost of institutional legitimacy.

Pre-trade integrity. Dynamic price bands modeled on LULD, pre-trade risk controls modeled on Rule 15c3-5, wallet-level position aggregation, automated kill switches, and VAR-style latency-window protections.

Market maker programs. AMM infrastructure preserved as the mathematical foundation for the long tail, formal DMM programs layered on top for high-volume contracts, tiered rebates keyed to quote quality, explicit compensation for binary adverse selection risk, and routing structures that keep flow on central order books.

Resolution infrastructure. Named data sources declared in advance, public audit trails, independent integrity review committees with good-faith and intent provisions, and pre-declared voiding conditions including latency-window protections.

Cross-venue surveillance. CAT-equivalent order tracking across wallets, venues, chains, and wrappers, starting with CFTC-regulated jurisdictions and extending through bilateral regulatory arrangements over time.

Regulators do not grant legitimacy. They ratify it. The venues that build market-grade controls first will define the terms the rest of the category gets measured against. Everyone else will be building to specifications someone else wrote.

In December, this desk asked whether prediction markets going mainstream without these controls was gambling in an investment-grade wrapper. The honest answer then and now is yes, without them. But the controls are buildable. The playbook exists. It was paid for, in systemic failures, over the last forty years, and in the ongoing operating experience of adjacent event-driven markets.

The first venue to build this becomes the reference market. Not just for prediction markets, but for how probability itself is priced, traded, and trusted.

That is what asset-grade means. That is what is worth building.

References & Sources

Regulatory Framework

- Report of the Presidential Task Force on Market Mechanisms (Brady Commission, January 1988)

- Limit Up/Limit Down (LULD) NMS Plan (SEC, 2012)

- SEC Rule 15c3-5: Risk Management Controls for Brokers or Dealers with Market Access (November 2010)

- SEC Rule 613: Consolidated Audit Trail (CAT)

- NYSE Rule 104: Designated Market Maker Obligations

- SEC Administrative Proceeding: Knight Capital Group (October 2013)

Academic Literature

- Hanson, R. (2003). Combinatorial Information Market Design. Information Systems Frontiers.

- Hanson, R. (2007). Logarithmic Market Scoring Rules for Modular Combinatorial Information Aggregation.

- Hanson, R., Oprea, R., Porter, D. (2006). Information Aggregation and Manipulation in an Experimental Market. Journal of Economic Behavior & Organization.

- Hendershott, T., Jones, C., Menkveld, A. (2011). Does Algorithmic Trading Improve Liquidity? Journal of Finance.

- Biais, B., Foucault, T., Moinas, S. (2015). Equilibrium Fast Trading. Journal of Financial Economics.

- Harris, L. (2003). Trading and Exchanges: Market Microstructure for Practitioners. Oxford University Press.

- O'Hara, M. (1995). Market Microstructure Theory. Blackwell Publishers.

Industry Events & Market Developments

- AlphaRaccoon and Google Year in Search Insider Trading Allegations (2024)

- Chaos Labs: Analysis of Wash Trading on Polymarket (October 2024)

- Inca Digital: Blockchain Transaction Analysis for Prediction Markets

- Polymarket Acquires QCX to Secure CFTC-Registered Path (October 2025)

- InTrade: CFTC Enforcement Action (2013), SEC EDGAR Records

- PredictIt: CFTC No-Action Letter Revocation (2022)

Resolution & Adjudication Precedent

- ISDA Credit Derivatives Determinations Committee: Greek Debt Restructuring (2012)

- Hovnanian CDS Manufactured Default: ISDA DC Structural Exploitation (2017)

- Betfair Exchange: VAR Rule and Event-Driven Latency Protections